After several years of active promotion of electric vehicles, increasing data indicates that buyer preferences are shifting in the opposite direction. This material summarizes the findings of the recent global Deloitte study and helps understand which types of powertrains people worldwide are considering for their next purchase.

Context: Market Expectations and Reality

In recent years, electric vehicles have received significant support — from expanding model lineups to subsidies and tax incentives. Meanwhile, the development of new vehicles with gasoline and diesel engines has noticeably slowed. However, the growth in supply and informational activity has not led to a comparable increase in sustained demand.

Sales of electric vehicles in several countries remain at low levels and in some cases even decline year-over-year, despite the introduction of new models and additional stimulus measures. This has become the starting point for a more attentive analysis of actual buyer sentiments.

What the Deloitte Study Shows

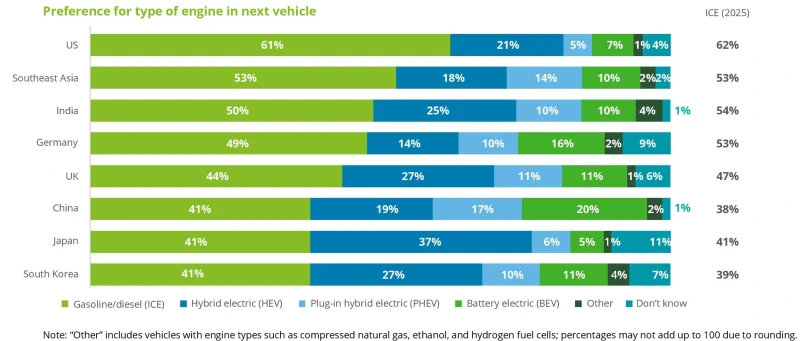

The Global Automotive Consumer Study 2026 from Deloitte covers key automotive markets worldwide: the US, Europe, China, India, Japan, South Korea, and Southeast Asian countries. One of the central questions concerned the type of powertrain that respondents would like to see in their next vehicle.

The results were clear. In most regions, the overwhelming majority of buyers are oriented toward vehicles with gasoline or diesel engines, including conventional ICE, hybrids, and plug-in hybrids. In the US, such options are chosen by about 87% of respondents, while fully electric vehicles are considered by only 7%.

Situation in Different Regions

The picture outside the US varies in details but not in overall logic. In China, interest in electric vehicles is higher, yet even there they are chosen by less than a quarter of potential buyers. In Germany, the share of supporters of fully electric drive is about 16%, in the UK — around 11%, in South Korea — about 11%, in India — around 10%, and in Japan — just a few percent.

These figures show that electric vehicles remain a noticeable but far from dominant part of the market. At the same time, most buyers still expect universality, predictability of operation, and clear ownership economics from a vehicle.

Reasons for the Shift in Sentiments

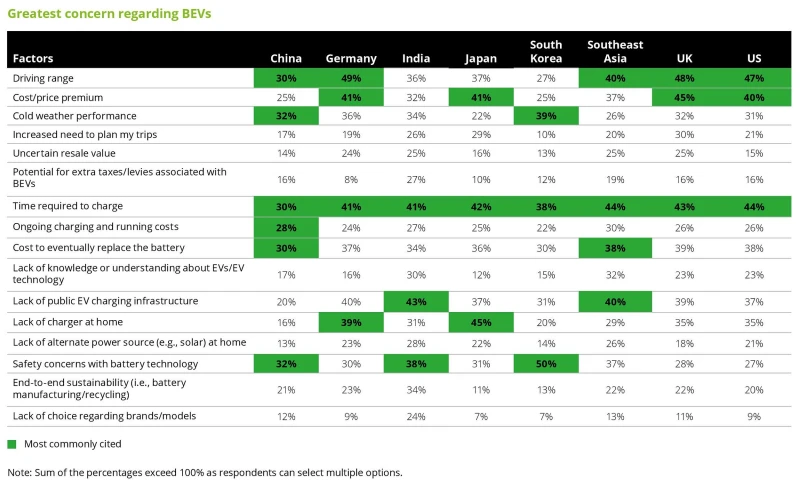

Deloitte notes that the turning point in attitudes toward electric vehicles has resulted from practical experience. Among the factors most often restraining interest are:

- limited range, especially in cold weather,

- long charging times at public stations,

- high cost of electricity for fast charging,

- rapid decline in residual value of vehicles,

- uncertainty regarding the resource and price of traction batteries.

Previously, from 2018 to 2022, a gradual and sustained shift in demand toward electric transport was expected, but recent surveys record the opposite trend — growing skepticism and a more balanced approach to technology selection.

What Matters to Buyers Today

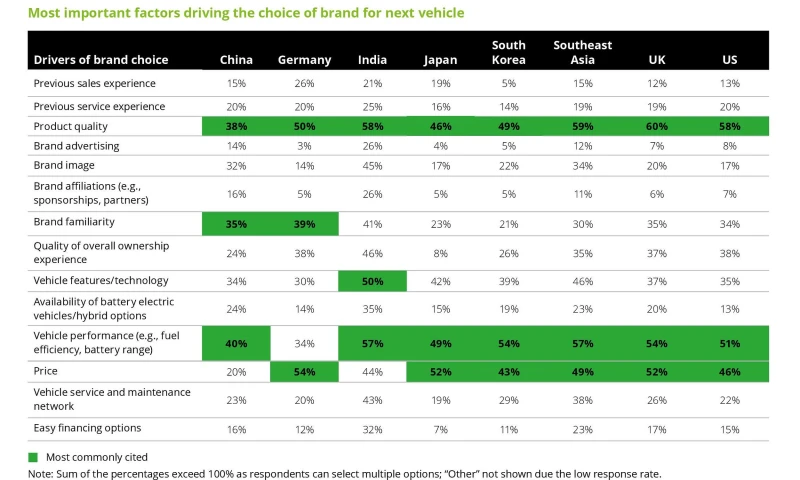

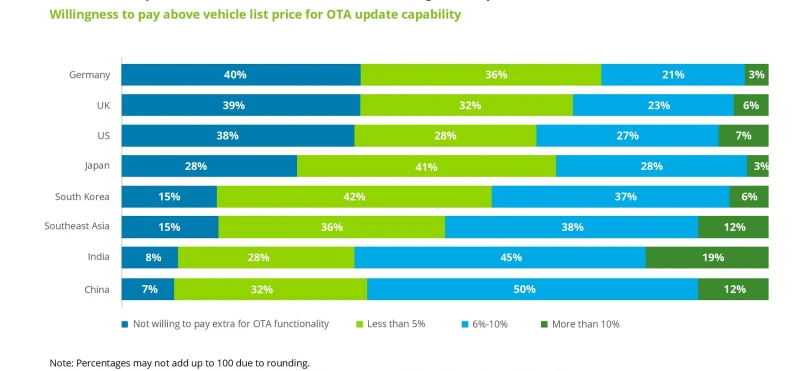

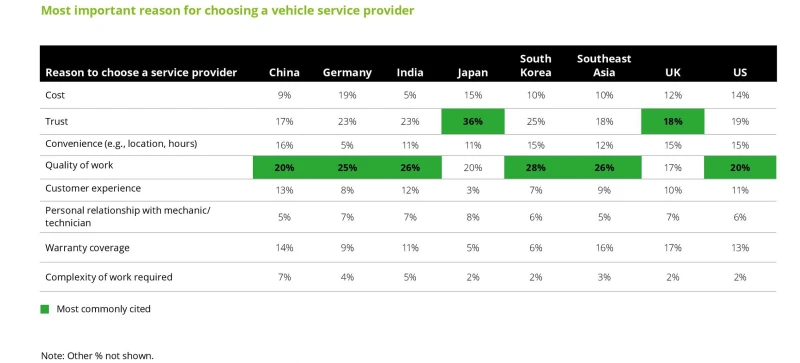

The study also shows that many manufacturer initiatives do not align with real customer requests. Online sales directly from the brand, paid software features, or over-the-air updates are not among the key selection factors. Much greater weight is still given to price, technical specifications, reliability, and accessible service.

Conclusion

Deloitte's data clearly demonstrates: expectations of a mass and rapid transition to fully electric transport do not match current buyer sentiments. Worldwide, most people still view gasoline and diesel vehicles as the basis of their mobility. For automakers, this is a signal of the need to consider real market preferences rather than focusing solely on forecasts and strategic declarations.